Fintech

In a business environment that demands slick customer onboarding, risk management and fintech identity verification, disrupt the market and position your business uniquely from traditional financial services.

Helping offer your customers a secure, trustworthy and truly global service, complete with cutting-edge user experience and full business protection.

Trusted by thousands of major brands around the world

Completely unique customer experience

Safeguard your business whilst setting yourself apart from competitors thanks to a more dynamic, frictionless and user-friendly UX.

Globally compliant and reputation of trust

Expand into new and emerging markets with ease, demonstrate a clear focus on safe and secure onboarding and total fintech compliance globally.

Seamless integration

Integrate any of our API solutions into your existing processes effortlessly with full real-time support from our dedicated industry experts.

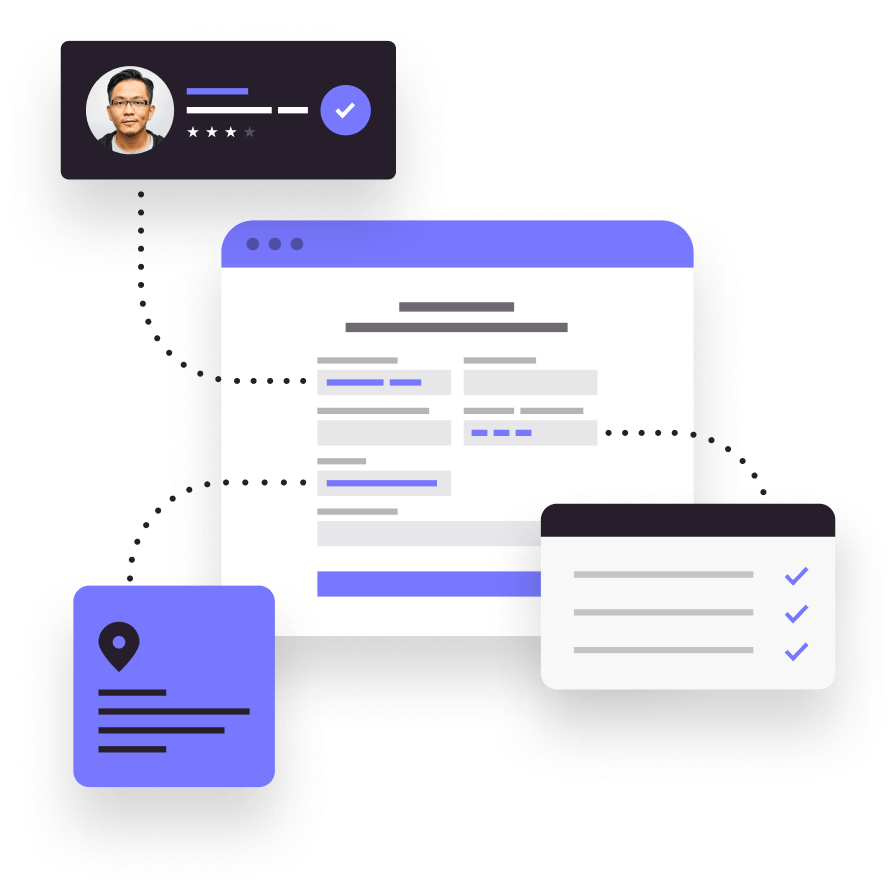

Identity Data Verification

Fast and safe onboarding checks

Onboard your customers with a simple, easy process which keeps them confident their data is secure. With minimal friction our solution optimises your identity risk and compliance (AML and KYC) procedures across multiple regions, providing your business with access to a range of comprehensive global data sources which are updated daily, making it simple to weed out fintech fraudsters and designed to support the regions you’re growing into.

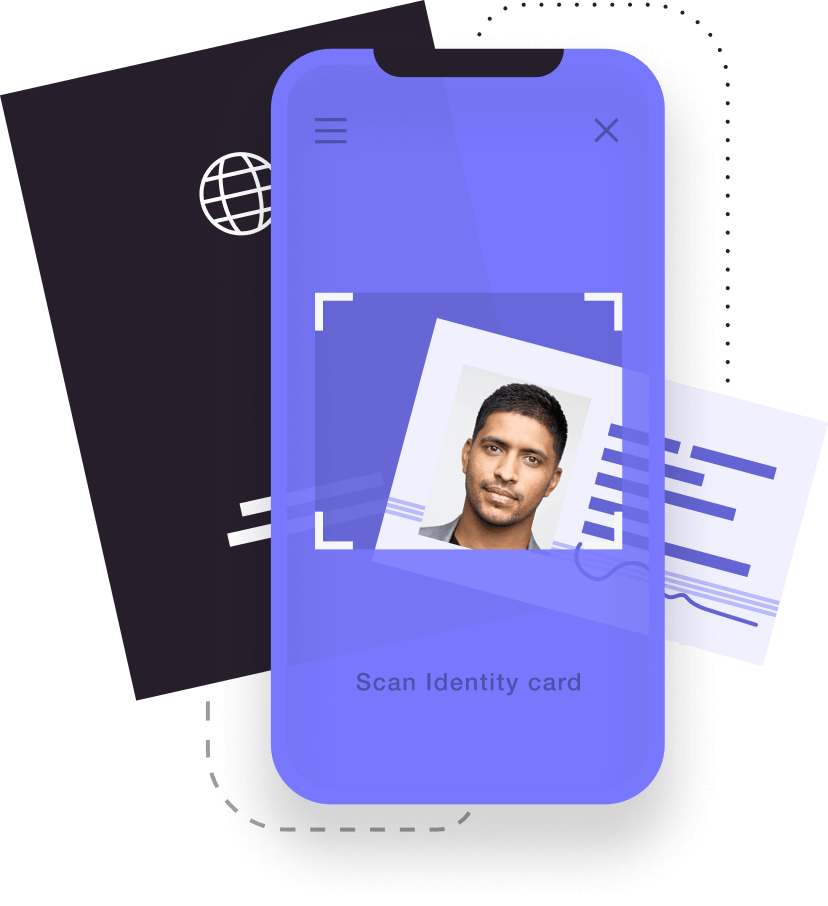

Identity Document Verification

Frictionless document authentication

Protect yourself against fraud and maximise efficiency with a cutting-edge document validation process that’s simple for customers all over the world. Using sophisticated biometric liveness checks, FaceMatch technology, smart capture technology and real-time human forensic document experts, our solutions ensure fintech onboarding processes are frictionless and safe.

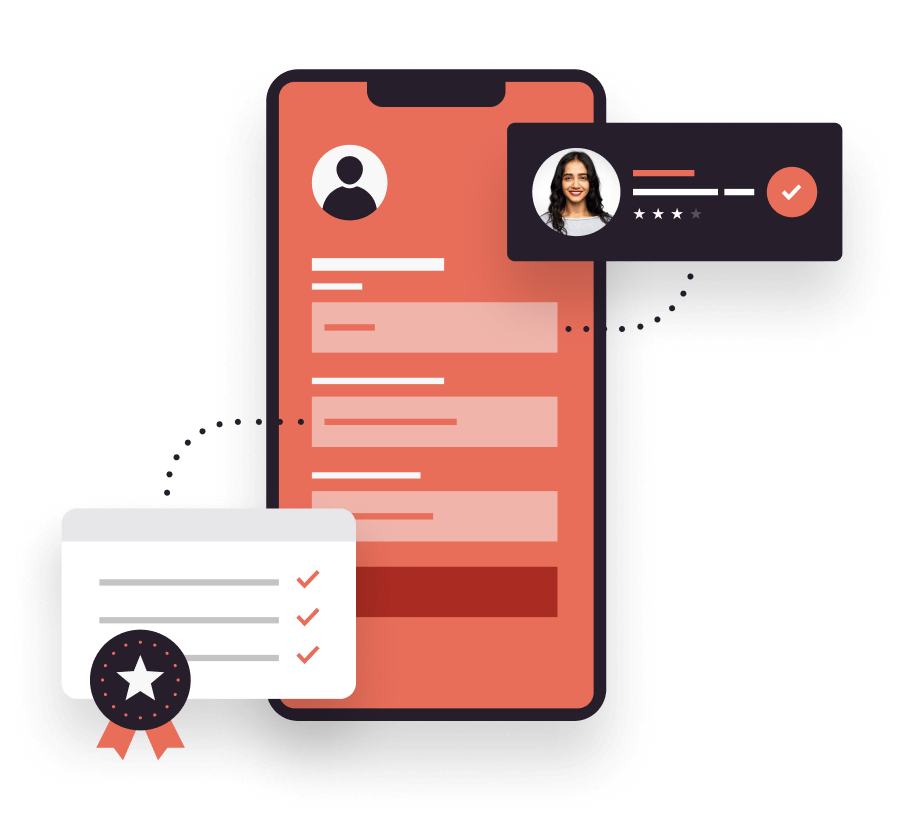

Application Fraud

Simple application fraud alerts

Safeguard your business against application fraud without impacting the customer experience. Using fintech AML and KYC compliance techniques, our easily-integrated solutions keep your business alert to all forms of application fraud, as well as false or stolen identities which are synonymous with money laundering.

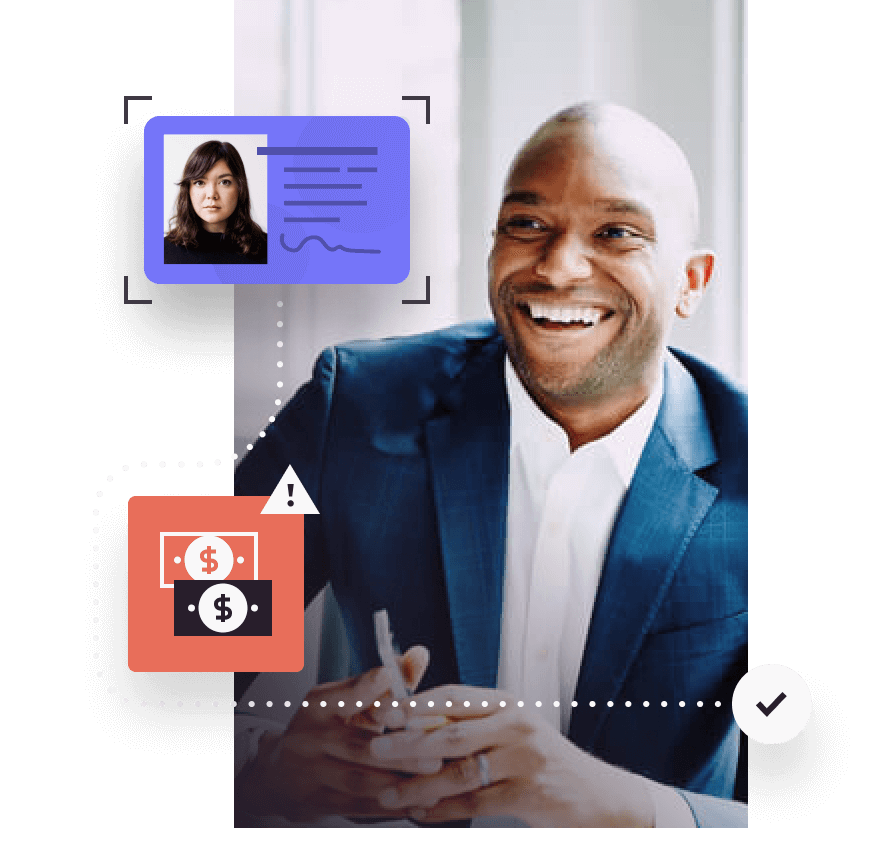

Transaction Fraud

Prevent fraud before it strikes

Fight transaction fraud with constant, intelligent monitoring based on your business needs - checking every transaction across every channel. Maintain compliance as your business grows globally, meeting all the necessary requirements for AML and counter terrorism funding.

Recommended products

Why choose GBG

At GBG, we take fintech identity verification and compliance management very seriously. Regardless of your location, business size or target market, our bespoke solutions can be implemented quickly and with no disruption to business. This means your organisation’s current identity verification processes can continue to operate seamlessly while our API integrations are implemented.

Each of our smart identity, fraud and location intelligence solutions help you to deliver first-class online experiences, while also ensuring you can verify the identity of almost anyone, anywhere in the world, at any time, meeting all global compliance requirements in the process.