KYC: What your business needs to know

Jonathan Jensen

Know your customer – everything you need to know about KYC, from what it is to how it benefits your business. We highlight the importance of KYC and how your businesses can strengthen KYC compliance and build long-lasting relationships with customers based on trust.

What is KYC?

It’s important to verify that your customer is who they say they are and that you can trust them. Equally, you want customers to trust your business. You only want to do business with good customers and customers want safe transactions with companies.

For regulated businesses, know your customer or KYC compliance is an important part of the process of establishing trust between a business and a customer. While KYC compliance is a requirement in regulated industries, however, knowing your customer is a best practice for any business looking to transact and interact with trust and confidence.

KYC? AML? What’s the difference?

Anti-money laundering (AML) refers to a wide set of laws and regulations mandating steps that financial institutions and other regulated industries must take to prevent criminals from depositing or transferring funds that come from illicit activity – money laundering. AML regulations are designed to stop the financing of terrorism and other illicit activities. Regulated industries must not knowingly or unknowingly aid these activities.

Know your customer (KYC) refers to the KYC checks that a company carries out to ensure their customers are who they say they are and do not pose a risk to the business.

While these terms are often used interchangeably, anti-money laundering (AML) is the collective term for a range of regulatory compliance processes businesses must have in place of which KYC compliance is one. KYC checks typically fall into three activities.

- Customer due diligence (CDD)

- Enhanced due diligence (EDD)

- Continuous Monitoring

"Knowing your customer is a best practice for any business looking to transact securely and any brand wishing to build trust and confidence, meanwhile, expanding global regulations mean businesses looking to scale need to be mindful of KYC requirements."

Why does KYC matter?

Regulation is evolving globally, driving the need for KYC compliance. KYC requirements are becoming more stringent in tackling financial crime, privacy and consumer rights. With an increasing number of processes coming under the AML spotlight, higher penalties and higher customer expectations for data privacy, companies need to stay on top of what’s expected of them in the countries in which they operate.

Knowing your customer is a best practice for any business looking to transact securely and any brand wishing to build trust and confidence, meanwhile, expanding global regulations mean businesses looking to scale need to be mindful of KYC requirements.

Stay on top of ever-changing regulatory requirements with all-encompassing protection.

Which businesses need to run KYC checks?

The types of business that must meet KYC compliance varies between jurisdictions. There’s a common misconception that KYC requirements only apply to the financial services industry. While these businesses are well represented, AML regulations and KYC requirements cover many industries, including:

- Financial services:

- Asset managers

- Banks, building societies and credit unions

- Consumer credit services

- Crypto exchanges

- Money transfer services

- Payment institutions

- Safety deposit services

- Other industries

- Accountants and auditors

- Art dealers (high value)

- Estate agents and letting agents

- Financial advisors

- Gaming operators

- Lawyers

- Tax advisors

"The UK’s Office for National Statistics found a 14% increase in total crime in the year to September 2021, driven by a 47% increase in fraud and computer misuse, which surged during the Covid pandemic."

What are the risks of fraud?

PwC's Global Economic Crime and Fraud Survey 2020 contacted 5,000 companies across 99 territories. Respondents reported financial losses totalling an eye-watering $42bn, in addition to the reputational damage to brand and loss of market share.

While the digital economy creates huge opportunities for individuals and the economy, it also creates new avenues for fraud. In a recent report, the UK’s Office for National Statistics found a 14% increase in total crime in the year to September 2021, driven by a 47% increase in fraud and computer misuse, which surged during the Covid pandemic.

Our State of Digital Identity Report 2022, reveals that as people have become more reliant on the internet for everyday tasks since the pandemic began the prevalence of identity fraud has spiked. Of the 2000+ consumers surveyed, almost one in 10 (9%) fell victim to identity fraud in the past year.

As fraud continues to rise and become more complex, businesses need to have robust KYC checks in place to prevent and reduce the risk of identity fraud.

What are the business benefits of KYC?

Every regulated business has a responsibility to avoid being implicated in money laundering or associated crime. Even if formal KYC requirements don’t apply to your business, however, it’s still an offence to aid or abet money laundering. So, why risk it?

KYC compliance aside, however, conducting KYC checks is still a smart business decision bringing some important business benefits:

- Consumer confidence

Your customers are concerned about fraud and are more likely to trust your business if you take their identity security seriously. - Brand protection

Failing to run KYC checks can put your brand in the spotlight for the wrong reasons and turn off both prospective customers and investors. - Smooth customer onboarding

Effective KYC checks balance fraud prevention with a smooth customer experience removing friction and frustration.

"The best identity verification solutions are configured and automated based on the risk profile of your business to ensure KYC compliance."

When should my business run KYC checks?

If your business is in a regulated industry, you’re required to run a risk assessment that will determine which KYC checks must be carried out and when. This assessment covers the risks inherent in your business, relating to your customers, markets in which you operate, products, services, transactions and delivery channels.

Based on this assessment, your business must then establish processes to effectively mitigate and manage the risks at different moments in the customer lifecycle:

- customer risk assessment

- customer due diligence

- ongoing monitoring

- transaction monitoring

- suspicious activity reporting

The best identity verification solutions are configured and automated based on the risk profile of your business to ensure KYC compliance. For higher risks, KYC checks occur repeatedly throughout the customer lifecycle to ensure any suspicious transactions are flagged quickly and addressed.

Why are KYC checks at customer onboarding important?

Whatever the risk profile of your business, KYC checks when onboarding new customers offer a minimum defence against fraud. You need to make sure that the person who wants to be your customer is a real person. So, identity verification is crucial when onboarding new customers.

Good identity verification solutions can be configured to match the risk profile of your business, ensuring that you meet KYC requirements without complicating your customer experience or lengthening the onboarding processes.

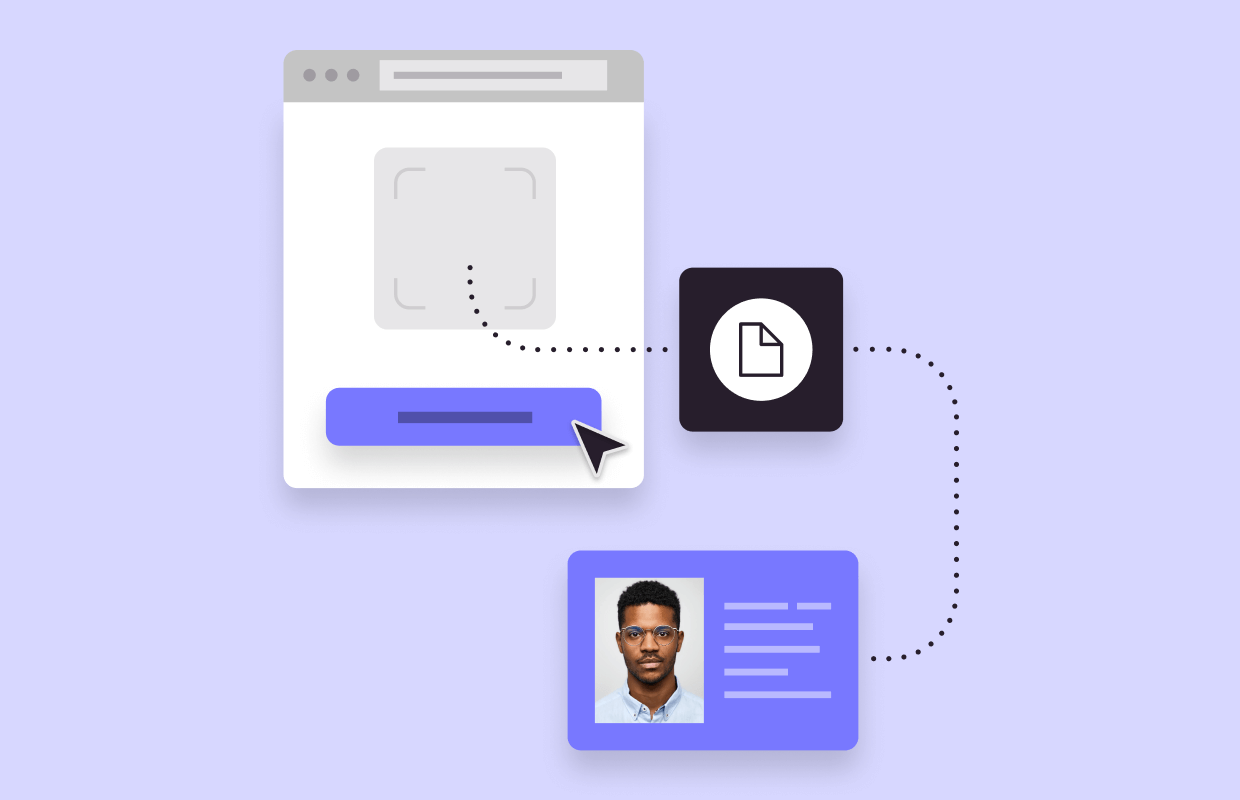

- Identity document verification

Scanning and capturing information from a government-issued identity document and authenticating the document as genuine is an important evidence-based approach to KYC checks. For accurate document identity verification worldwide, your business requires access to a comprehensive global database of identity documentation.

- Identity data verification

Combining document verification with checks of identity data against global data sources such as credit reference agencies and electoral registers helps to establish that person has made other transactions. Mobile and other alternative data can increasingly be layered into your KYC checks to ensure a better understanding of an individual.

- Identity authentication

As well as checking that this is a genuine identity, you need to check that it belongs to the person presenting it to your business. Facial recognition and liveness checks, for example, can compare a potential customer’s ID with their actual characteristics and physical measurements so you can trust they are who they say they are.

"If your business is in a regulated industry and you don’t meet KYC requirements, you can be fined by regulators and, in more serious cases, face criminal prosecution."

Fraud is always evolving. Maximise your defence against current and future fraud.

What is customer due diligence?

For regulated industries, customer due diligence (CDD) describes the type of identifying information your business must collect from customers to be able to confirm who they are. CDD covers business relationships with individual customers as well as business-to-business relationships.

The extent of CDD your business needs to carry out will vary depending on the type of customer. As part of a risk-based approach to KYC compliance, CDD must measure up to the level of assessed risk. For customer due diligence to meet KYC requirements, your businesses must:

- identify the customer

- verify their identity (minimum individual customer details)

- full name

- date of birth

- address

- nationality

- identify beneficial business owners (where relevant)

- verify the identity of each beneficial owner

- assess the purpose of the business relationship

What is enhanced due diligence?

Enhanced due diligence (EDD) is required for customer relationships assessed to be of higher risk. It refers to increased monitoring of the customer relationship and assessment of the background and purpose of transactions. For enhanced due diligence to meet KYC requirements for individuals, one (or more) additional steps may be involved:

- certified proof of identity and address

- notary check

- evidence of source of funds and wealth

- sign-off by a business director and money laundering reporting officer (MLRO)

First impressions matter in business. Make sure your customer experience is smooth and secure.

How to get your customer onboarding right

Creating a good first impression of your business is essential. If you want to avoid lost business, that means ensuring KYC checks in your customer onboarding experience maintain the low friction that customers now demand without compromising on KYC compliance or the risk of fraud.

The best identity verification solutions are tailored to your business, configured to match the risk profile of your industry and built to automatically accept, decline, and refer decisions, wherever your customer is located in the world, speeding up the onboarding process for your legitimate customers.

If your business is multinational or has plans to scale, you need to ensure your customer onboarding process meets global regulatory requirements, adapts to changing standards and compliance needs in the markets you serve without the need to constantly re-engineer, and easily meets industry regulations when entering new markets.

What happens if my business doesn’t make KYC checks?

If your business is in a regulated industry and you don’t meet KYC requirements, you can be fined by regulators and, in more serious cases, face criminal prosecution. What’s more, those penalties for non-compliance could make the headlines, which can cause damage to your brand and the reputation of your company, discouraging prospective customers and potential investors in the future.

How GBG can help you with KYC compliance?

Keeping on top of ever-changing regulatory requirements can be tricky. Our KYC solutions make KYC compliance management as simple as possible for your business, helping you to do your customer due diligence anywhere in the world. It’s our business to help you to build online customer relationships based on trust while keeping the fraudsters at bay without impacting the customer experience.

Sign up for more expert insight

Hear from us when we launch new research, guides and reports.