Affordability checks for gambling operators

Screen for vulnerability without adding friction

GBG’s Geo-Affordability data offers a unique picture of UK demography, which will allow us to make instant, accurate assessments that tailor our products to ensure that customers’ activity is affordable as well as fun.

Trusted by thousands of major brands around the world

Protect players

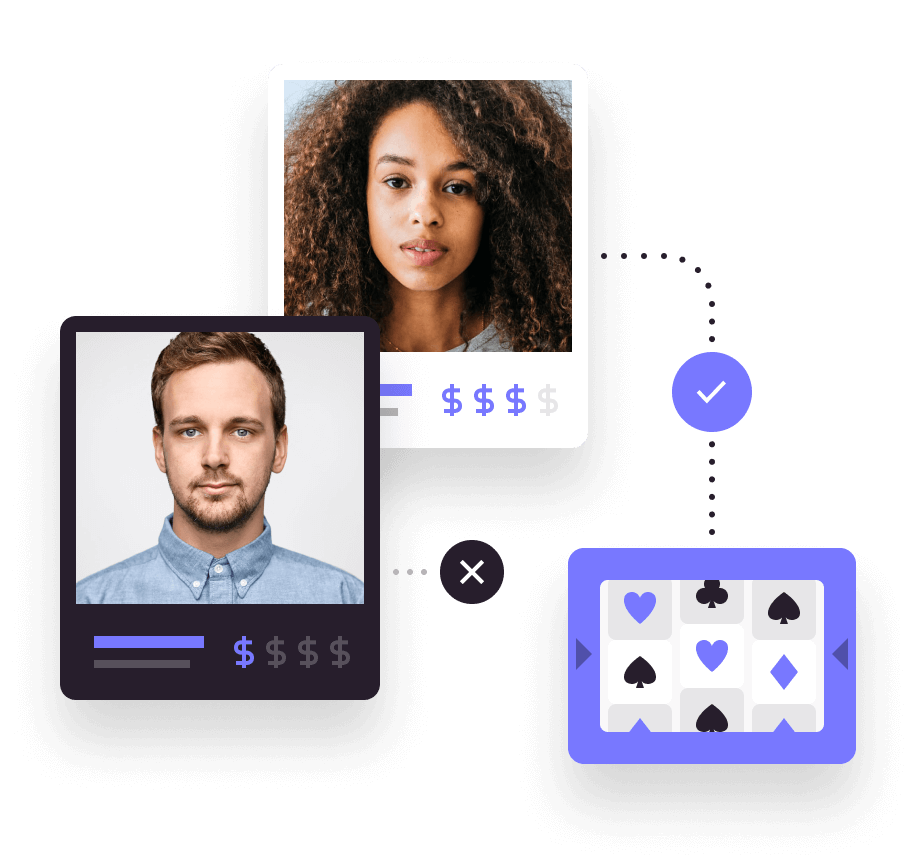

Understand a player’s financial circumstances in real-time with ‘Red Amber Green’ statuses that make affordability screening easy

Seamless player experience

Run affordability checks without additional input from players, ensuring a seamless experience and minimal customer drop-off

Informed decisions

Layer our range of affordability checks to make better decisions based on your approach to risk and existing player onboarding processes

Identify vulnerable players

Get a flexible and fully configurable approach to identify vulnerable players. Use postcode-level data to screen at onboarding layered with individual affordability checks further into their journey or at key trigger points.

Flexible integration

Integrate at any point during your player journey. Our fully automated, layered solution delivers an accurate and complete view of player affordability. It’s easily consumed alongside age and AML checks, and all stored within a single, granular audit trail.

Compliance driven

Integrate with your existing processes and audit trail easily and satisfy regulators.

GBG Affordability Solution

Expert insights and customer stories

GBG in conversation with Bess Matthews

Rebekah Jackson talks with Bess Matthews, Product Manager at GBG. They discuss how we developed the Affordability Solution to run alongside our current age, AML and identity verification checks so that gaming operators can undertake affordability checks without additional friction in customer experience.

GBG in conversation with Chris Elliott

GBG in conversation with Lee Willows

Rebekah Jackson talks with Lee Willows, CEO of Young Gamers & Gamblers Education Trust (YGAM). They discuss how Lee's former addiction to gambling drove him to set up the charity to help educate young people about problematic gaming and gambling.

Get in touch

Find out how our Affordability Solution can help enhance your commitment to responsible gambling. Request a demo today.